For millions of senior citizens and families across the United States, Medicare is not only a healthcare program—it's a vital lifeline. However, in recent years, a crucial trend has emerged, which is a steady rise in Medicare premiums. This has increased the healthcare costs and directly impacted the home budgets of the senior citizens, many of whom live on fixed incomes. As premiums rise, so do worries about affordability, access to care, and long-term well-being.

Here, I have tried to explore the problem and highlight the emotional and financial burden these changes bring and provide actionable solutions to help seniors.

Rising Medicare Premiums and Financial Strain on Seniors

Medicare, the healthcare program that started in 1965, was designed to provide health insurance to individuals aged 65 and older, as well as certain younger people with disabilities. While it managed to serve its purpose and is still continuing, the cost of Medicare is steadily rising, especially when it comes to monthly premiums. This has put a lot of financial pressure on the senior citizens. According to recent data, settlement costs for Medicare-involved claims have surged by 52% between 2018 and 2024, surpassing the general inflation. And this cost is posing a direct impact on the monthly expenses of senior citizens.

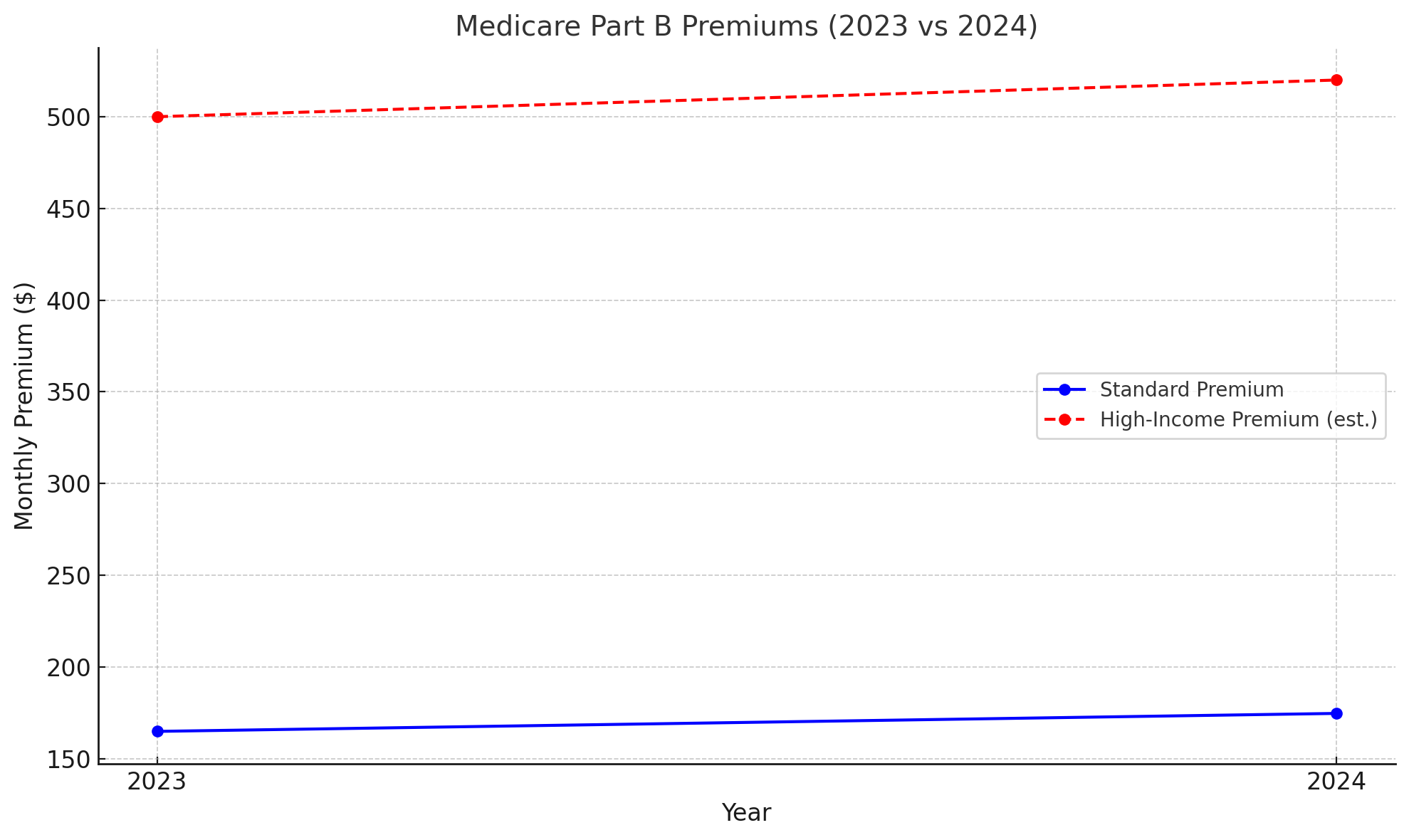

For example, Medicare Part B premiums have seen a consistent increase in the monthly premium, reaching $174.70 in 2024. Additionally, other expenses such as deductibles and copayments continue to rise, making it difficult for seniors to afford necessary medical care.

Understanding Medicare Premiums

Medicare consists of several parts:

- Part A (Hospital Insurance): Generally, premium-free if you or your spouse paid Medicare taxes for at least 10 years.

- Part B (Medical Insurance): Covers doctor visits, outpatient care, and preventive services.

- Part C (Medicare Advantage): Offered by private insurers combining A & B, often including Part D.

- Part D (Prescription Drug Coverage): Also offered through private plans with varying premiums.

In the above parts, Part A is usually free, Part B premiums are mandatory for most, and that’s where the biggest cost hikes have occurred.

Here is the data

According to the Centers for Medicare & Medicaid Services (CMS), the standard Part B premium for 2024 rose to $174.70 per month, up from $164.90 in 2023. That’s nearly a 6% increase in just one year. For high-income earners, premiums can exceed $500 per month.

Similarly, Part D plans saw a rise in premiums, with the average monthly cost reaching around $34.50, depending on coverage level and insurer.

These costs have made a severe dent in the senior citizens with fixed incomes of $1,500 to $2,000 per month.

Real-Life Struggles of Seniors Facing Rising Healthcare Costs

With these changes in numbers, it also shows the struggle of senior citizens, who worked their whole lives, paid taxes, and planned for retirement, are now finding themselves burdened by rising Medicare premiums and unpredictable healthcare costs.

This financial strain caused by rising Medicare premiums forces many seniors to make difficult choices. Such as delaying essential medical treatments, while others struggle to afford prescription medications. A study found that other costs for seniors aged 65-68 dropped from $1,646 to $1,230 after policy changes, but many still face financial hardship.

Many personal stories highlight the severity of the issue. Many seniors express concerns about their ability to maintain their health while managing their budgets. Some have had to cut back on other essential expenses, such as food and housing, to afford their healthcare costs.

Mary, a 74-year-old widow living in rural Ohio, receives about $1,800 in Social Security each month. She also has to cover rent, groceries, medication, and medical visits. With her Part B and Part D premiums increasing, her out-of-pocket expenses went up by $60/month in 2024 alone.

“I started skipping meals to afford my prescriptions,” Mary says. “I never thought it would come to this.”

Her story is not unique.

Many senior citizens have to make a hard choice between healthcare and essentials.

Many seniors, like Mary, are faced with impossible decisions:

- Should I refill my prescription or pay the electric bill?

- Can I afford that necessary surgery, or should I delay it?

- Is it safe to skip a checkup?

These trade-offs are dangerous. Skipping medication, delaying treatment, or avoiding medical visits can lead to more serious (and costly) health issues down the road.

Mental Health and Emotional Toll

The emotional impact of these financial pressures is also high. Constant anxiety about bills, feelings of guilt when asking children for help, or even depression from isolation are common among seniors under financial strain.

In a 2023 AARP survey, 62% of seniors expressed concerns about affording healthcare over the next five years. That’s more than half of our elderly population living in fear of their medical future.

Managing Medicare Premiums and Protecting Your Health

Though the challenges are real, there is hope. Seniors and caregivers can take steps to minimise Medicare costs, budget wisely, and access support systems designed to ease the burden.

1. Review Your Medicare Plan Annually

Every year, Medicare plans change—new benefits, costs, and providers. Take time during Medicare Open Enrollment (October 15 - December 7) to:

- Compare different Part D and Medicare Advantage plans.

- Check if your medications are still covered.

- Evaluate whether switching plans could reduce premiums or out-of-pocket expenses.

Use tools like the Medicare Plan Finder at medicare.gov for easy comparison.

2. Apply for Extra Help (Low-Income Subsidy)

If your income is limited, the Extra Help program could reduce your Part D premiums, deductibles, and co-payments. In 2025, this could save beneficiaries up to $5,300 annually.

To qualify:

- Income below $22,000 for individuals or $30,000 for couples.

- Limited resources (savings, stocks, etc.)

- Apply via the Social Security Administration at ssa.gov.

3. Look into Medicare Savings Programs (MSPs)

MSPs can help pay Part B premiums and sometimes deductibles and co-insurance. There are four types:

- Qualified Medicare Beneficiary (QMB)

- Specified Low-Income Medicare Beneficiary (SLMB)

- Qualified Individual (QI)

- Qualified Disabled and Working Individuals (QDWI)

Each has specific income/resource limits. Contact your State Health Insurance Assistance Program (SHIP) for help applying.

4. Explore Community Resources and Nonprofits

- Local organisations and nonprofits often provide

- Free medication assistance

- Transportation to medical appointments

- Health education and wellness programs

- Financial counselling for budgeting

Organisations like Meals on Wheels, PACE (Program of All-Inclusive Care for the Elderly), and local Area Agencies on Ageing offer valuable services at little or no cost.

5. Create a Healthcare Budget

- Smart budgeting is key. Consider:

- Listing all monthly expenses.

- Separating needs vs. wants.

- Setting aside a healthcare emergency fund, even if small.

- Using budgeting apps designed for seniors or low-income households, like GoodBudget or YNAB (You Need A Budget).

Even minor savings (cutting streaming services or switching phone plans) can help offset rising Medicare premiums.

6. Consider a Medicare Advantage Plan

- Some Medicare Advantage (Part C) plans offer:

- Zero-dollar premiums

- Dental and vision benefits

- Prescription coverage

- Wellness programs

While the above options can provide relief to some, these plans could lower overall healthcare costs if your preferred doctors are in-network. Carefully compare plans using CMS Star Ratings to gauge quality.

Looking Ahead: What Can Be Done at the Policy Level?

While individuals can take action, systemic changes are also needed.

Recent Policy Proposals

The Inflation Reduction Act of 2022 included provisions to cap out-of-pocket costs for prescriptions at $2,000 starting in 2025.

The federal government is now allowed to negotiate drug prices for select Medicare-covered medications, which could slow premium growth.

What You Can Do

- Stay informed about legislation impacting Medicare.

- Join advocacy groups like AARP or Medicare Rights Centre.

- Contact local lawmakers and share your concerns—your voice matters.

Conclusion: Take Charge of Your Medicare and Your Health

The rise in Medicare premiums is more than just a line item on a budget; it is a pressing issue that requires proactive solutions. It’s a personal challenge that affects the health, stability, and peace of mind of millions of senior citizens. It is possible to manage healthcare costs; seniors must learn and know budgeting strategies, seek assistance programs, and stay informed about policy changes. By taking these steps, they can better manage their healthcare expenses and maintain their well-being.

Step: If you're a retiree or approaching retirement, review your Medicare plan, compare options annually, and seek guidance to reduce unnecessary expenses.

- Apply for financial help programs like Extra Help or MSPs.

- Reach out to community resources for guidance and support.

- Talk to a licensed Medicare advisor to ensure you’re not overpaying.

Let’s ensure that ageing with health and peace of mind remains a reality, not a privilege. Most importantly, there are people, programs, and services ready to help. Have questions about your Medicare options? Visit medicare.gov for personalised assistance.